Opportunity cost is a fundamental concept in economics that plays a crucial role in decision-making processes. It refers to the value of the next best alternative that is foregone when a choice is made. Understanding opportunity cost is essential for individuals, businesses, and policymakers as it helps in evaluating the trade-offs involved in any decision. […]

Factors of Production: A Comprehensive Exploration

The factors of production are the essential resources used in the creation of goods and services. Understanding these factors is fundamental to economics, as they form the backbone of any economic system. The four primary factors of production are land, labor, capital, and entrepreneurship. Each of these factors plays a crucial role in the production […]

Understanding Work Motivation: A Comprehensive Exploration

Work motivation is a critical aspect of organizational behavior and human resource management that influences employee performance, satisfaction, and overall productivity. It refers to the internal and external factors that stimulate individuals to take action towards achieving their work-related goals. Understanding work motivation is essential for organizations aiming to foster a productive work environment, enhance […]

Understanding Statistical Population: A Comprehensive Exploration

In the realm of statistics, the concept of a statistical population is fundamental to the design and interpretation of research studies. A statistical population refers to the entire group of individuals or items that share a common characteristic and from which a sample may be drawn for analysis. Understanding the nuances of statistical populations is […]

Understanding Statistical Samples: A Comprehensive Exploration

Statistical sampling is a fundamental concept in statistics that involves selecting a subset of individuals, items, or observations from a larger population to make inferences about that population. The purpose of statistical sampling is to gather data that can be analyzed to draw conclusions, make predictions, or inform decision-making without the need to study the […]

Imperfect Competition: A Comprehensive Exploration

Imperfect competition is a market structure that deviates from the ideal of perfect competition, where numerous buyers and sellers operate under conditions of complete information and free entry and exit. In imperfect competition, the characteristics of the market lead to varying degrees of market power among firms, resulting in outcomes that can differ significantly from […]

Understanding Perfect Competition: A Comprehensive Exploration

Perfect competition is a fundamental concept in microeconomics that describes a market structure characterized by a large number of buyers and sellers, homogeneous products, and free entry and exit from the market. This theoretical model serves as a benchmark against which other market structures, such as monopolies and oligopolies, can be compared. Understanding perfect competition […]

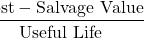

Depreciation: A Comprehensive Exploration

Depreciation is a fundamental concept in accounting and finance that refers to the reduction in the value of an asset over time due to wear and tear, obsolescence, or age. It is an essential aspect of financial reporting, tax calculations, and asset management, as it affects a company’s financial statements and tax liabilities. Understanding depreciation […]

Responses to Abiotic Factors

Abiotic factors are the non-living components of an ecosystem that influence the living organisms within it. These factors include physical and chemical elements such as temperature, light, water, soil, and atmospheric conditions. Understanding how organisms respond to these abiotic factors is crucial for comprehending ecological dynamics, species distribution, and the overall functioning of ecosystems. This […]

Embryonic Development: A Comprehensive Exploration of the Stages, Processes, and Significance in Human Growth

Embryonic development is a complex and fascinating process that transforms a single fertilized egg into a fully formed organism. This intricate journey involves a series of well-coordinated events that include cell division, differentiation, and morphogenesis. Understanding embryonic development is crucial not only for biology and medicine but also for comprehending the fundamental principles of life. […]

The Female Reproductive System: An In-Depth Exploration

The female reproductive system is a complex and vital part of human anatomy that plays a crucial role in reproduction, hormonal regulation, and overall health. Understanding the structure and function of this system is essential for comprehending how it contributes to fertility, menstruation, pregnancy, and childbirth. This article will provide a comprehensive overview of the […]

Pregnancy: A Comprehensive Overview

Pregnancy is a remarkable biological process that involves the development of a fetus within a woman’s uterus. It is a complex journey that typically lasts about 40 weeks, divided into three trimesters, during which significant physiological, hormonal, and emotional changes occur in the mother’s body. Understanding the stages of pregnancy, the changes that occur, and […]

Mammary Glands: A Comprehensive Exploration of Structure, Function, and Importance in Lactation and Beyond

Mammary glands are specialized exocrine glands found in mammals, responsible for the production and secretion of milk. This unique feature is one of the defining characteristics of mammals, providing essential nutrition to offspring during their early stages of development. The study of mammary glands encompasses various aspects, including their anatomy, physiology, hormonal regulation, and clinical […]

Understanding NATO: Structure, Purpose, and Global Impact

The North Atlantic Treaty Organization (NATO) is a military alliance established to promote collective defense and security among its member countries. Founded in 1949, NATO has evolved over the decades to address changing geopolitical landscapes, security threats, and the complexities of international relations. This article will provide a comprehensive overview of NATO, including its history, […]

Understanding Qualitative Variables: A Comprehensive Exploration

In the realm of statistics and research, variables play a crucial role in data collection, analysis, and interpretation. Among the various types of variables, qualitative variables—also known as categorical variables—are fundamental for understanding non-numeric data. Qualitative variables are used to represent characteristics, attributes, or qualities that cannot be quantified numerically. They are essential in fields […]